by Aussie Firebug | Mar 9, 2022 | Net Worth

I publish these net worth updates to keep us accountable, have others critique our strategy and show that reaching financial independence in Australia is very doable without winning the lotto, having a high paying job or inheriting a wad of cash. The formula to be able to retire early is simple, the hard part is being consistent and sticking to a plan for many years. The table at the bottom details our entire journey from being $36K in debt all the way until we reach 🔥

The wife and I surprised my parents with a trip to Daylesford in February for the old man’s birthday. It was a bit of a combo trip to also see my sister who has recently moved to Bendigo.

Daylesford

Mrs FB has dropped to a 4-day working week this year and the extra day off has really been a game-changer for her. One of the best parts about having a long weekend every week is being able to plan little 3-day get-aways (I’m ironically finishing up this post on one said getaway). We left Latrobe Valley early on Friday morning and came back on Sunday night. I even managed to fit in a coffee with a Firebug reader in Ballarat which was really nice.

That’s the beauty of slowly scaling it back. Even just one extra day in the week gifts you back 52 days a year (not exactly 52 days with all her teacher holidays but you get the idea). Even if it’s just to book appointments and get some stuff done. Half the time Mrs FB sets aside the Friday to organise and prep for the following week and we wake up Saturday morning with all the chores done. It’s a really nice way to enjoy the weekend instead of trying to cram in everything on Sunday just to wake up Monday morning and start the process all over again.

I also had my first BJJ (Brazilian Jiu-Jitsu) tournament in Feb which was such a crazy experience.

For those who haven’t heard of BJJ before, Wikipedia describes it as:

Brazilian Jiu-Jitsu is a martial art and combat sport based on ground fighting and submission holds. BJJ focuses on the skill of taking an opponent to the ground, controlling one’s opponent, gaining a dominant position, and using a number of techniques to force them into submission via joint locks or chokeholds.

Or as I like to explain it to my wife… “You’re basically trying to kill the other bloke without striking” 😂

I first started training BJJ in late 2018 after me and my mate finally decided to pull the trigger and actually go down to a local MMA gym and give it a go. We were huge fans of the UFC and MMA in general but had never trained a martial art (I’ve done a bit of boxing but nothing serious).

I only trained for a few months in late 2018 before Mrs FB and I left to live overseas for two years. I originally wanted to continue my training in London but life and travelling just got in the way. I was lucky to get in a few gym sessions and a run during the week let alone BJJ training.

What attracted me to BJJ was the ‘problem solving’ nature of it. I’ve gravitated towards puzzles my whole life. I love chess, my favourite video game of all time is StarCraft which is extremely strategic and my professional work in data is literally solving technical problems for money.

A lot of people think martial arts can be too violent and just for meatheads but there’s also a softer more spiritual side that’s deeply connected with meditation and yoga (think Shaolin Monks for example). I like to think of meditation as a form of martial arts and struggle against your own mind, yoga is a martial art against your body and BJJ is the physical manifestation against another person. They’re all related and I’ve been told that a lot of top BJJ practitioners are right into mediation and yoga too.

We came back home in 2021 and BJJ training was high on my list to get back into. It took me a few rolls to bounce back to my previous level and other than the lockdowns we had last year, I pretty much have had a solid 12 months of training plus the 3 months before our Euro trip. The next step was to put our training into practice because my mate and I always had aspirations to compete.

It’s one thing to train, but it’s another to actually go out there and wrestle someone giving 100%. To say it was nerve-wracking leading up to the comp is putting it lightly haha.

The day of the tournament was a relief because I had trained pretty hard 6 weeks leading up to it and I had been having a bit of trouble sleeping (probably overthinking everything that could go wrong lol).

We had 4 people from our club in the comp and the way it works is there are different divisions depending on your skill level, weight and BJJ style.

I was competing in both Gi (the pyjama looking outfit 🥋, also called a Kimono in Judo) and no-Gi (tights and rash vest, pictures below) in the 77kg white belt (beginner) division.

It was a round-robin competition which I would highly recommend to anyone looking to compete. I really like the round-robin format because you’re guaranteed 4 matches even if you lose each one. Our coach has told us stories when he was competing that he would drive all the way up to Melbourne, lose the first match in a knockout tournament and have to drive all the way home 🤪.

I got to the comp, weighed in and started stretching and warming up. Our best guy from the gym (a blue belt) was up first and I was in the coach’s chair which is basically a spot for someone to yell out helpful things and let them know if they’ve scored points or not.

There are three ways you can win.

- The match finishes (5-minute matches) and you score more points (points are awarded for dominant positions)

- Your opponents submit from a choke or joint lock (they’ll usually tap or verbally submit)

- You choke your opponent unconscious and the ref steps in

So the match starts and it’s pretty competitive but the guy from our gym eventually loses on points after 5 minutes. I was surprised to see him limping really bad once the match finished and even more surprised to see his foot had turned black and blue… he broke his foot somehow during the match 😱

So this was just about the worst thing to have happened before my first match because you could imagine what that did to my confidence. Here I was, brand new to tournaments and already crapping my dacks. And then our best guy goes out there and breaks his foot… 😐

I helped him to the side where he was ushered off in an ambo, and then my name was called to mat 7.

My opponent and I stepped on the mat and the ref yells:

“Are you ready? Are you ready?… FIGHT!”

I don’t think I’ve ever had an adrenaline dump quite like it before. I know there’s a ref and rules but in the heat of battle without any prior experience, you just forget everything.

There are actually some similarities between holding your nerve in sports and keeping it together during a market downturn. How often do we hear from seasoned investors that buying during a downturn is one of the best things you can do. Buy when there’s blood in the streets etc. But it’s a different story when you’re actually in the thick of it.

I had trained and refined my strategy for 6 weeks leading up to the comp. But when my match started, my opponent gave me a different puzzle to solve than what I had been practising. This threw me off my game completely and I needed to make an adjustment but I didn’t have the experience/confidence to do so. That’s why you always see the best UFC fighters and boxers making adjustments mid-fight. They recognise when something isn’t working and under extreme pressure are able to try something different to solve the puzzle.

I fumbled around for most of the match and then somehow managed to land a double leg takedown to secure 2 points and win my first match. After that first one, I felt a lot more comfortable and I got into my groove during the next few matches.

I finished the comp coming 3rd in Gi (🥋) and 1st in no Gi (🚫🥋). My two mates both took home 2nd in their respective divisions which made it a very successful day for our school (other than our blue belt friend).

Here are some pics from the tournament.

My first opponent had neck tats… I was so nervous lol

Me almost getting guillotined

I’ve also been hitting up the local MTB trails with my nephew lately. It’s such a luxury to be able to go riding during the week when no one is there.

MTB riding at the pines

My nephew sending it!

And lastly, we finally got around to putting in the new front garden. I can’t believe how expensive plants are 💸 but must say that it’s looking 100 times better already. Really excited for the trees and bushes to grow a little.

New garden

Net Worth Update

A pretty boring update for February.

Our shares portfolio went up ever so slightly and Super dropped a few grand. I also had a smidge over three weeks off in January which meant my income for February was pretty low. All of that combined meant that we went slightly backwards in Feb from a financial point of view BUT I feel from a happiness point of view, things have never been better and that’s the important metric 😁

No changes to the FIRE portfolio.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

It’s becoming clearer and clearer that inflation has well and truly hit our tightass household. I’ll probably keep it eye on it for a few more months before anything official but I dare say that we’ll be increasing our FIRE number of $1.25M soon. I’ll write an article about it after a few more months I reckon. Inflation was always included in our numbers but not at the level it seems to be right now. I’m aware that CPI is officially 3.5% (as of writing this article) but our basket of goods has definitely gone up more than that.

I have been religiously tracking our expenses for over 7 years now and have a pretty decent dataset I could use. It would be interesting to see how much certain areas of our spending have changed throughout the years. I swear we only use to spend around $350 bucks a month on groceries. Now it’s closer to $600.

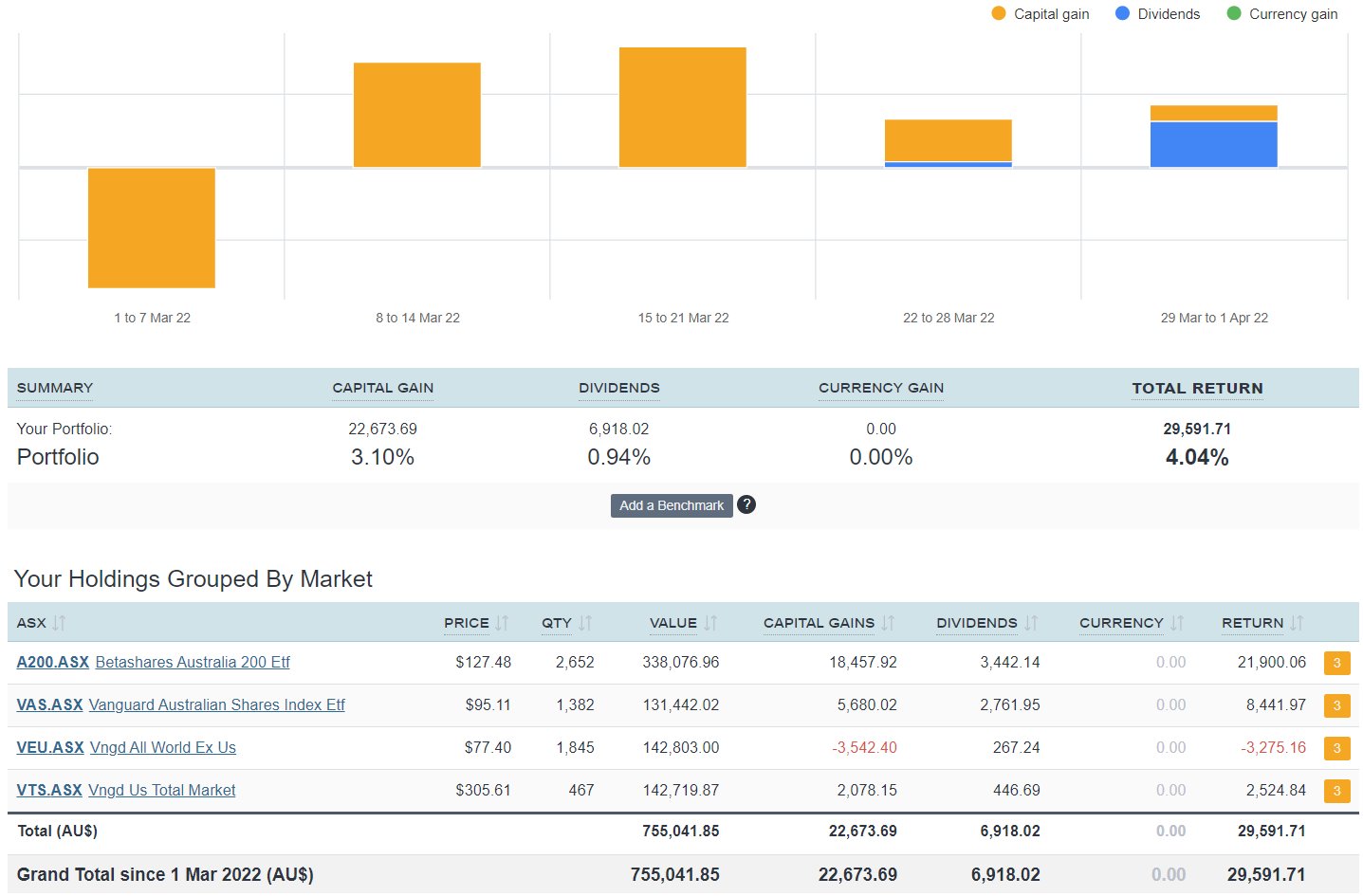

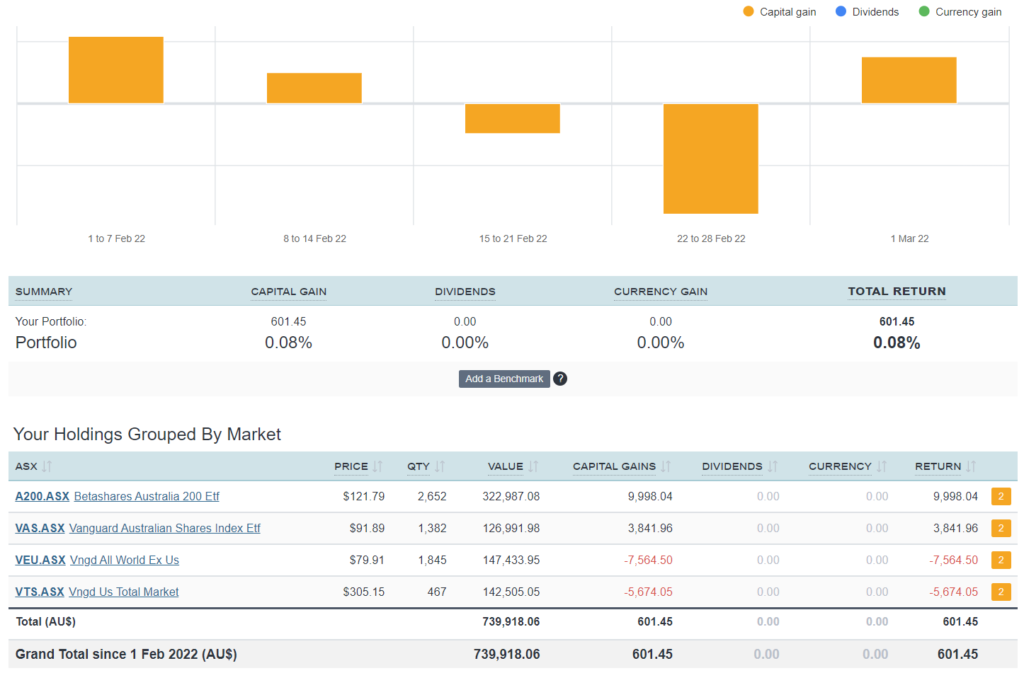

Shares

The above graph is created by Sharesight

No purchases in February. Building up a bit of a cash buffer for a new car atm

Networth

by Aussie Firebug | Feb 16, 2022 | Net Worth

I publish these net worth updates to keep us accountable, have others critique our strategy and show that reaching financial independence in Australia is very doable without winning the lotto, having a high paying job or inheriting a wad of cash. The formula to be able to retire early is simple, the hard part is being consistent and sticking to a plan for many years. The table at the bottom details our entire journey from being $36K in debt all the way until we reach 🔥

We kicked off 2022 with some travelling which almost didn’t happen.

Mrs FB and I are aspiring parents and basically, everyone has told us to get in as much travel/activities/sleep-ins as possible before a future newborn comes onto the scene (we’re not currently expecting atm). The original plan back in August last year was to get in one more overseas trip before the potential avalanche of responsibilities from parenthood hit us 😂.

It was originally going to be Japan because we missed it due to Covid in 2020. But as the months went by, the restrictions weren’t easing up enough for us to risk it plus Omicron went bananas later on in 2021. There’s was the whole ‘getting stuck’ over there risk, hotel quarantine (already paid that once 🙃) and probably the most likely risk of them all… getting a half baked Covid experience.

I’ve been thinking about what the world is going to be like after Covid for a while now because it doesn’t take a rocket scientist to know it’s not going to be the same.

Think about how much airport security changed after 9/11. A lot of the world was affected by that event. And whilst 9/11 was unprecedented, Covid is really on another level in terms of impact and severity which is saying a lot.

I mean… what sort of restrictions are going to be sticking around post-Covid? Will masks become the norm (people voluntarily wearing them)? Number restrictions on large gatherings?

I remember how much fun I had at Octoberfest back in 2019. Will that be the last Octoberfest of its kind… ever? There’ll be more festivals in the future but I’m not sure they’ll be the same. Our descendants might be able to look at photos of our generation and easily know if the picture was taken pre or post-Covid.

It’s a bizarre thing to think about really.

Anyway, back to our travel struggles…

So we axed Japan because things were getting worse, not better and I’m pretty sure Australia wasn’t even on the ‘allowed’ list to enter the country 😅.

We flirted with the idea of New Zealand but they didn’t want us either 😢.

So we ended up deciding that we’d have a look around our own backyard instead. Having never been to Western Australia, I was a bit disappointed that the borders were still closed because it was our preferred destination… oh well, next time I guess. South Australia and Tassie were next up and we were in luck with these states coming from Vic. I remember getting a slight scare in mid-December when the SA/VIC government started to mandate a combined total of 3 Covid tests before entry. It was originally 1, then it went to 2 and then 3 and I thought “Ahhh man, it’s just a matter of time before they lock us out”. Thankfully that didn’t happen and were able to cross the border to start our January holiday.

We hit up Adelaide first and I was really impressed by the city. Beautiful gardens and parks, great spots to eat and drink, plenty of recreational activities, world-class beaches just up the road and affordable housing from what I’ve heard. It’s no wonder that Adelaide always ranks highly in those ‘worlds most livable cities’ studies.

I really enjoyed hiring the orange bikes/electric scooters to see the city. Was a lot of fun.

Adelaide Gardens

Adelaide Riverbank

Adelaide Open

Gorgeous winery just out of Adelaide called ‘Down The Rabbit Hole’

I also caught up with Loch aka Captain Fi.

The Cap’s Sky Garden

Co-Captian FI aka Angel

He was kind enough to help organise an impromptu FIRE meeting in Adelaide with less than 48 hours notice 😅. I think we had around 10-15 people come and go throughout the night and it was one of my highlights of January. Getting out there and meeting Aussie’s from the FIRE community has been one of my goals since returning home. Last year was hard with all the restrictions but I’m really hoping 2022 can be the year of FIRE meet-ups! I’m planning on hosting a few in Gippsland and maybe even Melbourne 🙂

A big thanks to everyone who attended the Adelaide FIRE meet-up. I’ll be back one day for sure!

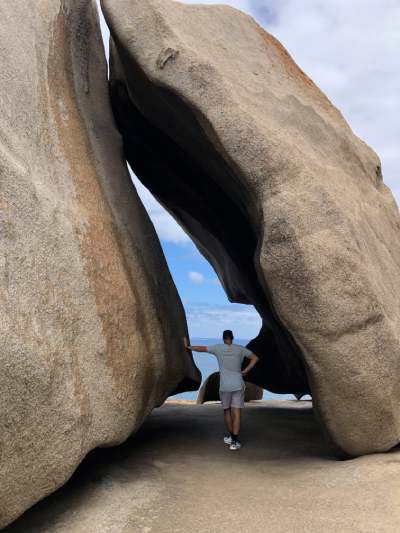

We headed to Kangaroo Island (KI) next but unfortunately had caught a bout of bad weather and couldn’t do everything we had hoped. It was still a lot of fun though. Here are a few shots.

Remarkable Rocks

Admirals Arch

After SA we headed to Tassie to meet up with our family and do some sightseeing.

I had already been to Tassie about 7 years ago and I remember being really impressed with Hobart’s Salamanca markets and Mona museum so I didn’t mind going there again. Plus we were exploring around the island to heaps of places I hadn’t been to before anyways.

Here are a few shots.

Royal Tasmanian Botanical Gardens

Enjoying a Frothy @ The Hanging Garden

Wineglass Bay

St Helens MTB Trails

We had such a great time sightseeing around Tassie.

I also managed to have another small impromptu FIRE meet up at Preachers in Hobart. It was such a cool little bar with a great bar garden and I really enjoyed meeting more people from the community. A big thanks to everyone who came out and had a drink with us.

We got around on more of those orange scooters in Hobart which I really liked. Seeing a city on those scooters or a bike is 100 times better than driving around IMO. One of my favourite things about Hobart and Adelaide is that you can get anywhere in the city on a bike/scooter within the hour. Having lived in a bigger city like London I really appreciate the smaller size of our Australian cities. Even Melbourne and Sydney are a lot more compact compared to New York, London, Tokyo etc.

I remember being a bit shocked when we went to a friends place for drinks in London once. We punched the address into City Mapper and the designated route said it was going to take over an hour to get there 😐. That’s a crazy amount of time to get from one place to another in the same city. I still maintain that riding a bike is the quickest way to get around in London but even so, you’d have to be pretty fit for some return trips around the city and most people aren’t going to ride their bike to a party lol.

Speaking of bikes, I had no idea that the MTB scene in Tasmania was so prevalent. I’ve recently started to hit the trails with my nephews and it’s been an absolute blast! I managed to get Mrs FB on a bike and the trails at St Helen’s were awesome. I’d love to come back one day and hit up Blue Derby for sure.

Net Worth Update

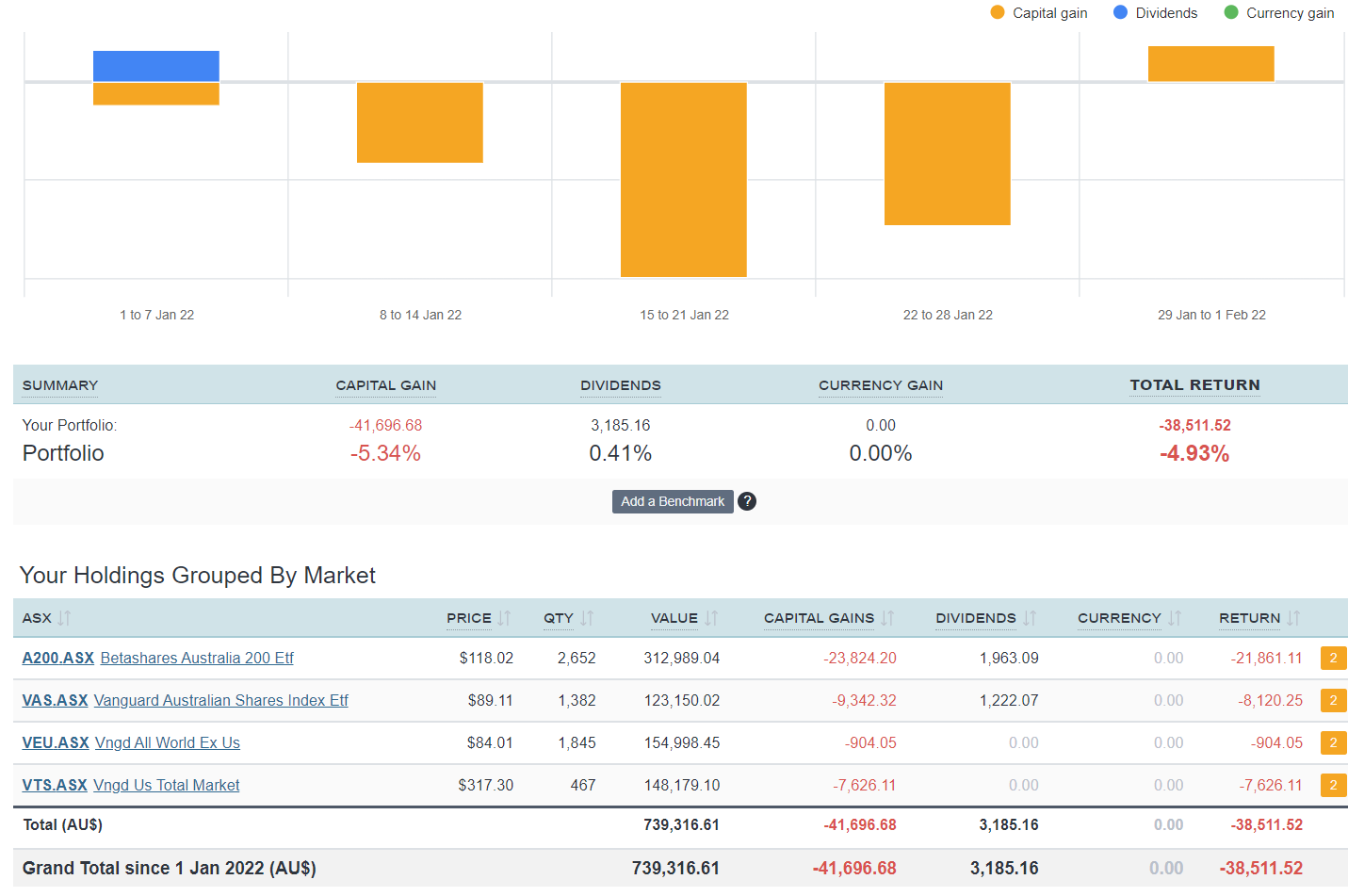

The cruel mistress of market timings punished me in January after I obviously angry her by holding onto our lump sum for too long 😂

After lump summing > $200K at the start of Jan, the markets started to dip and went south pretty quick with a slight recovery towards the end of the month.

This dip in the markets is the main reason for the drop in our net worth this month. Our share portfolio took a beating along with Super.

It was also a really expensive month again (inflation maybe?) and we didn’t save that much money.

Man, I forgot how much holidaying and eating out can really add up quick. A key difference these days is us having a mortgage whilst holidaying. When we were in London, we could sub-let our room before heading off on an adventure for a few weeks. But these days, it’s a double whammy of expensive accommodation plus our mortgage 💸. It’s still been worth it IMO but just reinforces my point of view that owning a PPoR is bloody expensive and can really clamp you down financially and geographically.

No changes to the FIRE portfolio.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

Expenses continue to be really high for the second month in a row. This is mostly accounted for by our holidays but I’ve noticed our grocery bills have been insanely high over December and January. This is partly because I bought a new BBQ and have been hosting a lot of dinners with my mates. Playing host is super fun but can be really expensive too. Inflation has definitely had an impact on our expenses though.

I remember back in 2018 we would consistently spend around $4K – $4.5K a month for everything. It’s been hard to know what our baseline is atm because last year had so many one-off purchases (wedding, PPoR). It might take another year to see what it will look like. Will be interesting to see how this graph changes over the coming months.

Shares

The above graph is created by Sharesight

We didn’t make any purchases in January. We are saving a bit of extra cash in preparation for buying a new car later this year. The 2nd hand car market is still crazy and I’ll like to put it off for as long as possible but it’s something we’ll have to buy eventually.

Does anyone have any recommendations for a solid family car (SUV or wagons are preferred)? I’d love to hear about them in the comment section 🙂

Networth

by Aussie Firebug | Jan 28, 2022 | Classics, Popular Article, Uncategorized

Reflection time.

I started full-time work at the end of 2011 and discovered the concept of financial independence (FI) sometime in 2012 after reading Rich Dad Poor Dad by Robert Kiyosaki.

That book (and the concept of FI) changed my life.

It wasn’t until a year after reading that book that I stumbled across Mr Money Mustache and the FIRE movement, which again, changed my life.

10 years. That’s how long I’ve been chipping away at this goal. And a lot can change ya know. My mindset, goals, strategy, desires, priorities have all shifted throughout the last decade. I’ve been thinking a lot about the lessons I’ve learned throughout the journey. What worked? What didn’t? What’s the point of it all?

Let’s get it.

1. The ultimate goal is to be happy. Never lose sight of this

We’re starting this list with the most important lesson.

It’s a bit philosophical but it’s really important and it sets the tone for everything we do. Have you ever asked yourself the following question and really mulled it over?

“What do I want in life?”

Now, there are going to be thousands of different answers to that questions depending on who you’re speaking to but the common denominator will always be the same… a desire to feel joy/to be happy.

Going snowboarding is pretty obvious. That’s fun as hell! But going to the gym 3 times a week and lifting heavy shit is… less obvious. One involves instant gratification whereas the other is delayed by a series of uncomfortable painful sessions.

The driver and end result for both activities is still the same. To be happy.

This driver for happiness is behind nearly everything we do. But figuring out what sort of life is going to be fulfilling and bring us purpose is a personal journey. The sooner you identify the key drivers of your happiness, the quicker you can start to plan out your ideal life.

I know life sometimes feels really complicated and stressful but at the end of the day, we’re still just another animal on Earth whose needs and desires haven’t changed that much over the ~50,000 years we’ve been roaming around.

In 1943 an American psychologist called Abraham Maslow published a paper called “A Theory of Human Motivation” which included the now very famous Maslow’s hierarchy of needs.

Maslow’s hierarchy of needs

This hierarchy of needs is universal and transcends generations.

A spice merchant in Ancient Egypt 3100 BC would still need to cover each level on the pyramid (pun intended).

Start from the bottom and work your way up and don’t skip over the physiological needs either.

You’d be surprised how many people would feel 10X better by just getting a decent amount of sleep each night and eating the right foods.

How FIRE plays a part in helping you achieve a level of happiness can be explained better in lesson 2.

2. Find your why of FI

One of the biggest mistakes I have personally made and that I see all the time is people thinking that reaching financial independence will make them happy.

Spoiler alert. It doesn’t.

You need to find your ‘why’. Why do you want to reach FI? What will reaching FI mean for you? How will it make you happy?

Speaking from personal experience, FIRE resonated with me because whilst I quite enjoyed my job, I resented the fact that I was ‘stuck’ there 5 days a week. I didn’t like that feeling. And before I knew that FIRE was even a thing, I thought I was going to be in the cubicle for 40+ years 🤮

FIRE for me was about gaining more of the most precious resource we all have. Our time!

Free time is crucial for satisfying the top level of Maslow’s pyramid.

Money is just a man-made abstraction that doesn’t have any intrinsic value. We can leverage money to create more time and freedom in our lives. The most important part is knowing how to use this extra time and freedom to enrich our lives. Having a rock-solid ‘why of FI’ will help tremendously throughout your journey.

3. Master behaviours, not spreadsheets

This lesson took me many years to learn but it’s a goodie.

At the start of my journey, I was really attracted to the math and statistical side of FIRE. I loved reading about the Mad Fientist’s tax strategies (even though they were US based), MMM’s shockingly simple math behind early retirement and how the trinity study modelled over 80 years of data to come up with the 4% rule.

I used to seriously whip out the calculator on my phone at all hours of the night to crunch some number because I was obsessing over a 0.07% difference in management fees lol 😅.

But the further down the FIRE rabbit hole I traverse, the more I realise that spreadsheets, modelling and the math behind money management all meant diddly squat if your emotions and psychological makeup are not equipped to stay the course throughout your journey.

I’m not saying the numbers don’t matter, because they most definitely do. But our behaviours matter more.

“Financial success is not a hard science. It’s a soft skill, where how you behave is more important than what you know”

– Morgan Housel

There’s a great story that illustrates this point perfectly. In the intro of one of my favourite books, ‘The Psychology of Money’ by Morgan Housel. Morgan compares the stark contrast between an American Janitor called Ronald Read with a Harvard-educated Merrill Lynch executive named Richard Fuscone.

From his wiki page:

Ronald James Read (October 23, 1921 – June 2, 2014) was an American philanthropist, investor, janitor, and gas station attendant. Read grew up in Dummerston, Vermont, in an impoverished farming household. He walked or hitchhiked 6.4 km daily to his high school and was the first high school graduate in his family.

Read repaired cars at a gas station for 25 years and was a janitor at JCPenny for 17 years. He purchased a 2 bedroom house for $12K in 1959 and lived there for the rest of his life.

Friends of Read have been on record saying that he didn’t really get up to much. Some said his hobby was wood chopping and he lived a very low key life.

Read died in 2014 at the ripe old age of 92 which is where the plot thickens… Read made international news when he left over $6,000,000 (USD) to his local hospital and library. He also left over $2,000,000 to his stepkids too 🤯.

Read’s friends were dumbfounded. Where did he get all that money from?

Friends and family went looking for answers but they discovered there was no secret.

No lottery wins.

No hidden inheritance.

No hidden high paying secret spy job that he’d been keeping under wraps.

Read simply spent less than he earned and invested the rest in blue-chip stocks. The power of compound interest over decades did its thing and his low-income modest lifestyle managed to create a snowball worth more than $8M (USD) 🤯🤯🤯.

Ronald Read

Richard Fuscone was in the news a few months before the passing of Ronald Read for very different reasons.

Fuscone is basically the polar opposite of Read.

To say he’s well educated is putting it lightly. Check this out for a resume

I mean damn! That’s some serious alumni. And for those who don’t know, the University of Chicago offers one of the most prestigious MBA programs in the world. We’re talking about the upper echelon of prestigious education here.

Fuscone was a high flying executive who retired in his 40’s to pursue philanthropy and was once included in a “40 under 40” list of successful businesspeople. Fuscone got into financial difficulty in the mid-2000s after he borrowed heavily to expand his 18,000-square foot home that had 11 bathrooms, two elevators, two pools, seven garages, and cost more than $90,000 a month to maintain.

Then the 2008 financial crisis hit.

High levels of debt coupled with illiquid assets left Fuscone bankrupt.

A few months before Ronald Read passed and left his fortune to charity, Richard Fuscone’s home was sold in a foreclosure auction for 75% less than an insurance company figured it was worth… ouch!

Ronald Read was patient, Richard Fuscone was greedy. That’s all it took to overcome the enormous education and experience gap between the two.

So what’s the moral of the story?

It’s not about how smart you are, it’s about how you behave.

4. Getting wealthy is simple. Don’t overthink it

“Life is really simple, but we insist on making it complicated.”

– Confucius

Almost every single wealth-building strategy can be boiled down to three steps:

- Spend less than you earn

- Invest the surplus

- Wait

That’s it… seriously.

Now there’s an absolute chasm between ‘get rich quick’ schemes and long term investing but those three principles hold true 99% of the time. How you invest and what you invest in doesn’t particularly matter. As long as you’re outpacing inflation and have strong conviction in your investments you should be moving towards financial independence.

Fidelity Investments is a multinational financial services corporation based in Boston, Massachusetts. An interesting discovery was made when a customer account audit revealed that the best investors in their database were either dead or inactive.

How could that possibly be?

How could someone that’s not adjusting their portfolio to the macro and micro economic news, outperform savvy investors with all the latest up to date data at their fingertips?

Well, it turns out that when it comes to investing… less is more.

Which is very unintuitive and goes against basic logic.

See the thing is, almost no one can beat the market over the long term. But people (myself included) constantly fall for the trap of trying to add complex financial instruments to somehow gain an advantage over ‘unsophisticated’ investors. I’ve always been raised that you need to put in the effort to reap a reward. You have to work hard to get anything in life worth having. This is true for most things… just not when it comes to investing.

I created and now invest through a trust fund because I associated its complexity and mystic with higher returns.

I thought I needed to do something different. I needed to outwork others to have a good return.

Choosing an ordinary index fund and adding to it each month without doing anything else just felt…lazy lol. I had all this pent up excitement after discovering FIRE and I wanted to channel this energy into the journey. I wanted to work my ass off so I could reach FI as quickly as possible and I felt like boring lazy index investing is only for people who aren’t willing to put in the work. It’s taken me years to accept that not only is this approach perfectly fine, but it’s also statically the most optimal choice most investors can make.

Keeping it simple also frees you up to concentrate on what’s really important in life which ties into the first lesson, to be happy.

Complexity has the potential to steal your most precious resources; time and energy.

Money is the slave that works for us, not the other way around.

5. What’s measured is managed

If I could give only one tip to anyone looking to be better with their money, it would be to start tracking your expenses.

That’s it.

You don’t even have to do anything else. I promise you that you’ll save money and optimise your expenses within the very first session. You might think that you know what you spend money on but I’ll bet the house that the first time you analyse three months of expenses, you’ll be surprised.

This lesson falls under the umbrella of Lesson 3 ‘Master behaviour, not spreadsheets’. It’s been well documented that keeping track of any metric and reviewing it regularly has a psychological effect on humans that can help us improve a focus area.

If a sprinter wants to be faster, they’ll keep a record of how fast they run.

If a presidential candidate wants to become the president, they’ll record and analyse poll data with their team.

If Tesla wants to design self-driving cars, they’ll create, test and record different algorithms continuously and keep track of what did and didn’t work.

I think you get the idea.

What’s measured is managed!

And if you’re not measuring the most fundamental aspect of FIRE, you won’t be able to manage it effectively. Plenty of people can still reach FI without ever tracking their expenses but I know first-hand that measuring how much you’re spending and what your spending it on has a lot of positive psychological effects.

Some of the positives of tracking are:

- You regularly review where your precious dollars are being allocated to each month. Think back to lesson 1. ‘The ultimate goal is to be happy’. Is the stuff you’re buying ultimately making you happy?

- You can accurately calculate your current FIRE number? Guessing how much you spend each year to maintain your current lifestyle can create stress and anxiety when the time comes to retire. You’ll second guess yourself. Even though things can and will change throughout your life, if you’ve been tracking your expenses for a few years you’ll have a much better idea of what size portfolio you’ll need to retire.

- It’s super easy to trim the fat. Unused memberships and subscription services can sometimes fly under the radar. Reviewing expenses bring this wastage front and centre.

But be warned… overdoing this area can actually have negative consequences.

I used to be one of the worlds biggest tightasses (still pretty tight compared to most ‘normal’ people haha) but what I’ve found through the last decade of managing money is that the majority of people will find great success if they focus on the big four areas.

- Housing

- Transport

- Food/drinks (including alcohol)

- Holidays

Try to optimise these big areas and don’t kill yourself for paying for a haircut.

I’d say that the top one (housing) is probably the most important. Buying a huge house at a young age can stunt your wealth creation potential. Spending 50+% of your paycheck on rent has the same effect. You want to get your snowball up and running asap and let the compound interest do the heavy lifting over many years/decades.

If you optimise those big four areas to a point where you’re living a great life whilst having a decent savings rate it’s only a matter of time before you hit FIRE 🎉.

Ultimately, this lesson is super effective at improving your behaviours when it comes to money management.

6. Income potential is often overlooked

Over the last decade, I’ve met and spoken to a lot of people who have reached financial independence and there seems to be a common theme.

- They are good savers

- They have a higher than average income

The funny thing is that a lot of these people are actually below average investors. I heard all sorts of stories about how they might have lost money on a development, got swindled by a pyramid scheme or lost it all on a speculative stock. Yet they seem to reach FI decades earlier than most after eventually figuring out some form of investment that works for them.

The bulk of their wealth comes from a healthy savings rate powered by a high income.

For the first 7 or so years on my journey towards FI, I focussed solely on saving a whole lot of money and investing it in both real estate and stocks.

It wasn’t until I moved overseas in 2019 and more than doubled my hourly rate did I truly appreciate the power of earning more money.

I mean it’s pretty obvious, isn’t it?

The more you earn the more you can save and reach FI quicker. But for some reason, I always prioritised saving more and reading the same investing strategies over and over again making little tweaks here and there.

Having a high savings rate is really important. I reckon we managed to optimise our expenses after 1 or two years at most. After that, it’s pretty much been on autopilot. We have a pretty good idea about what brings us joy and where our dollars go.

I’ve spent way too long (especially at the start) obsessing over the ‘investing’ part of the FIRE equation. There are soooooooo many articles, videos, books, podcasts etc. that dive into all sorts of whizz-bang investing strategies that it can be confusing as hell.

It’s sorta like when you go to the Cheesecake Factory. Their menu is so bloody big and confusing that it can be overwhelming. I’ll try to read absolutely everything because I don’t want to order a meal and then have food envy because something better was further down the menu 😂. This is what’s known as analysis paralysis and a lot of people can fall prey to it (it personally took me years of reading about the stock market before taking the plunge).

It’s natural to feel like you need to know absolutely everything before dropping your money into the markets. But the truth is that we all make mistakes and the most basic concept of investing is buying things (real estate, stocks, precious metals, bonds etc.) that make you money. Don’t stress too much about building the perfect portfolio because I’m telling you it doesn’t exist.

Index investing appeals to so many people because it’s passive, diversified, low cost and provides a great return with little effort. Don’t overthink it. Work out a portfolio that you have strong conviction in and one that will allow you to sleep at night. Save your money and keep adding to the portfolio regularly.

If you still have time and energy to commit to FIRE after your expenses are under control and you’re happy with your investing strategy, I’d seriously start to look to increase your income.

High savings + high income + below-average investments

is better than

High savings + below-average income + above-average investments

Obviously, it does depend on how epic your investment returns are but generally the above is true from what I’ve personally experienced and seen over the last decade.

There are heaps of ways you can increase your income. I wrote about a few of them in this article here.

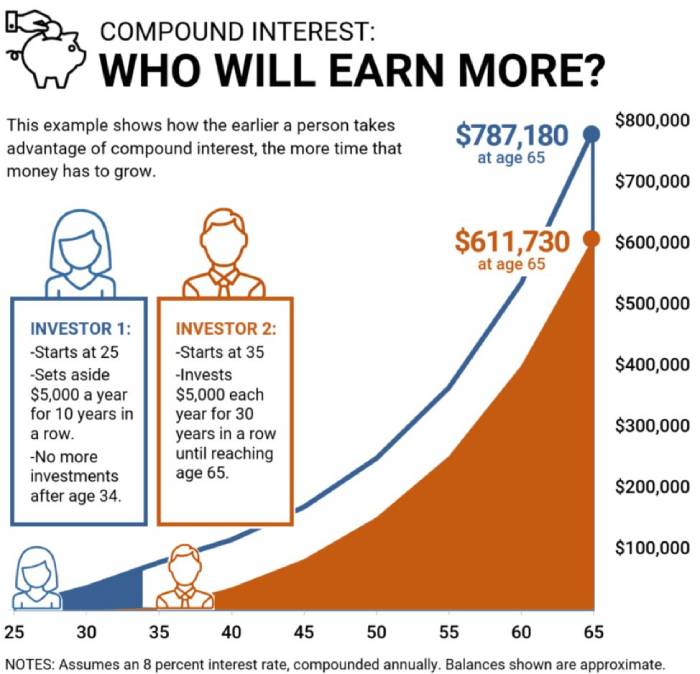

7. Compound interest takes years to notice

I learnt about the power of compound interest pretty early. There’s that famous story about two colleagues that’s told 100 different ways but it always illustrates the same point. Investing early and taking advantage of compound interest pays off in the long run.

This little graphic is one example.

Image Source: Mark Catanzaro

I’d like to think most people in the FIRE community have come across this (or something similar) before.

But most people (myself included) have a hard time truly appreciating the magnitude of compound interest and it doesn’t start to feel real until you’re near the end of your journey. There’s something about exponential growth that makes it difficult to grasp from an emotional point of view even when we understand the math. I think it has to do with most other things in life being linear. We do basic arithmetic almost every day in our lives but I don’t know anyone who can compute exponential growth without a calculator.

If we need half a dozen eggs for a recipe and know we already have 2 at home, that’s a simple subtraction problem that’s easy to think about on the fly and makes sense. If we choose to buy a car worth $10K instead of $15K. That’s an obvious savings of $5K which makes it easy to immediately appreciate on the spot.

But it’s hard sometimes to come to grips with putting away large sums of money now so the future you in 10-30 years can live a better life.

Here’s one of my favourite examples of exponential growth that you can play with your friends.

The story of the monthly coins.

If I gave you $1 each day in the month of January, how much money would you have at the end of the month?

Most people would be quick to shout $31 right.

But suppose I gave you $1 on the first day of January and double it every day until the end of the month ($2 on the second day, $4 on the third and so on), without cheating, try to have a guess in your head how much money you would have at the end of the month.

Take a few seconds to think about it and keep a mental note.

….

….

….

The answer is $2.1 billion dollars. That’s a billion… with a B 😱

Try this example with your friends to see what number they guess. 99% of the time they won’t get anywhere near the correct answer.

I use the example to illustrate the point that compound interest is not intuitive to grasp and it really only starts to take off in the later years. Speaking from experience, I really noticed compound interest once we had around $400K+ invested and our FIRE number is $1.25M for context.

Before that, it feels like you’re doing all the heavy lifting yourself through savings (which is pretty much what’s happening).

But boy oh boy it’s an amazing feeling when the freight train starts to pick up steam and suddenly your investments are making more money than you can save each month. After that, there’s no stopping it and you’ll feel like you’re almost cheating as you race towards the finish line.

8. Most people are really after semi-retirement

Every single financially independent person I’ve ever met, read about or listened to still ‘works’ and makes money outside their investments one way or another.

I’ve added talking marks to the letter ‘work’ because it’s not really traditional work but people can get really anal when it comes to the word retire. I’ve always interpreted RE (retire early) part of FIRE as the moment you quit your cubicle/wage slave job and pursue meaningful work that brings you purpose.

But this can be confusing because not everyone has something they’re super passionate about. There’s a large portion of the community that really likes the social aspect and comradery of their normal day job but just want a little bit more free time in the week to get stuff done and enjoy life.

Based on the emails I’ve been receiving for the last 7 or so years I’ve come to the following conclusion. Most people in the FIRE community are really just looking to work 2-3 days a week and maintain their current lifestyle with some passive income to cover the rest/set them up for retirement in their golden years.

And as someone who is currently only working 3 days a week, I must say that I’m becoming more convinced that semi-retirement is the sweet spot for the bulk of the community too.

Full financial independence is great and it’s what we should be aiming for later on in life, but building up a portfolio that kicks off enough passive income to free up one or two days a week can have astonishing results.

And the best part about compound interest is that the momentum you build up early on in the journey only gets stronger and can carry you all the way to full fledge FI without you needing to add to your portfolio after a certain point.

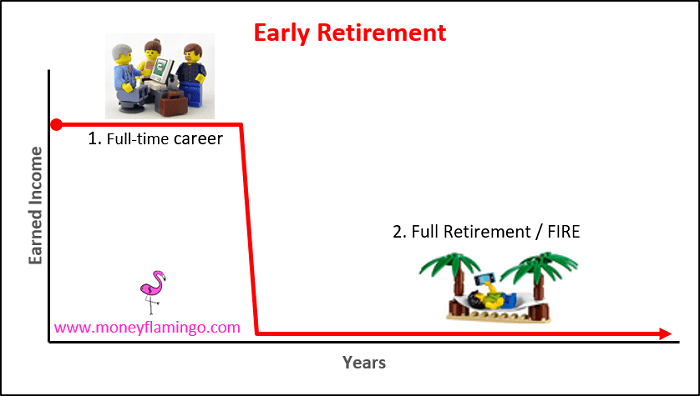

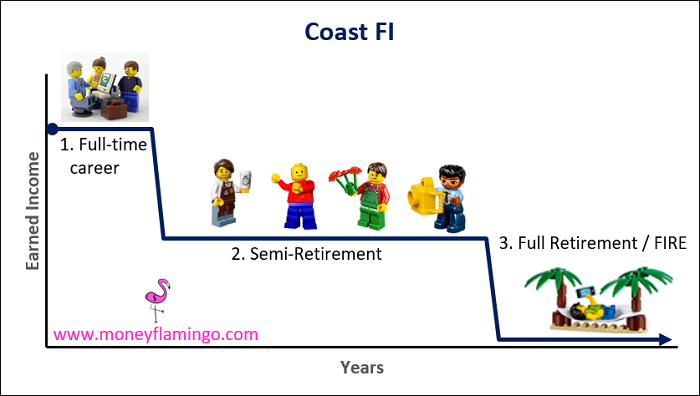

This concept is known as Coast FI or Flamingo FI and the end result is the same. Full financial independence.

But if you drop down to semi-retirement during your journey you’ll obviously not have as much money to contribute to your portfolio and won’t reach FI as fast.

Traditional FIRE. Source:moneyflamingo.com

Coast FI. Source:moneyflamingo.com

If you want to know more about coast FIRE I’d highly recommend you check out this article at the money flamingo blog (Aussie specific too!).

The odds of someone never working and making any sort of income outside of their portfolio ever again after reaching FIRE is incredibly low. I’ve been saying this for a few years now but the 4% rule is over-conservative in my book. Putting aside the fact that the author of the 4% rule has increased it to 5%, any additional income after you’ve reached FI completely blows out the modelling.

Let me give an example.

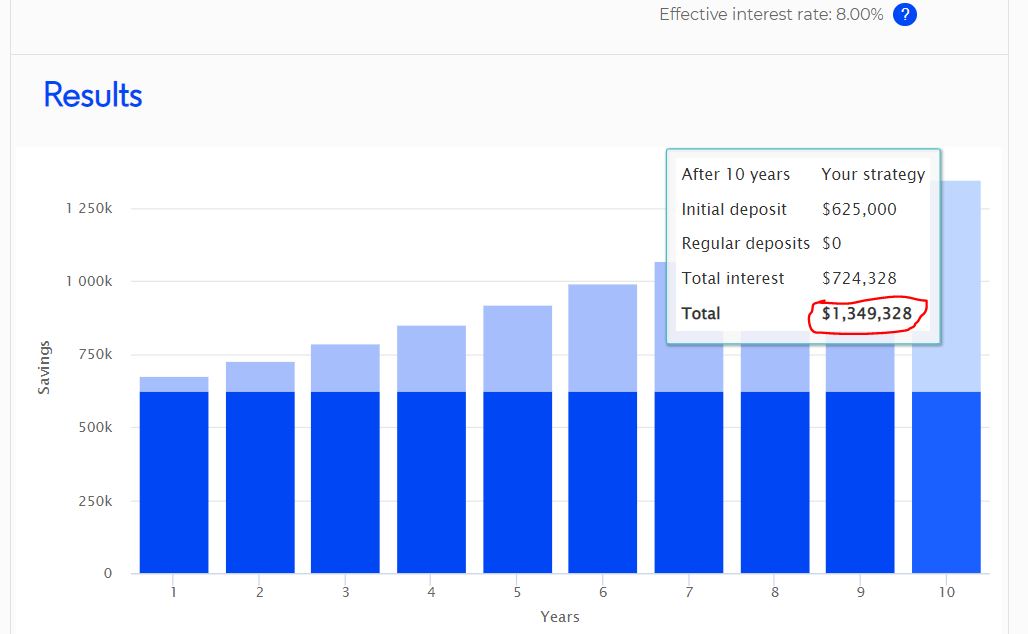

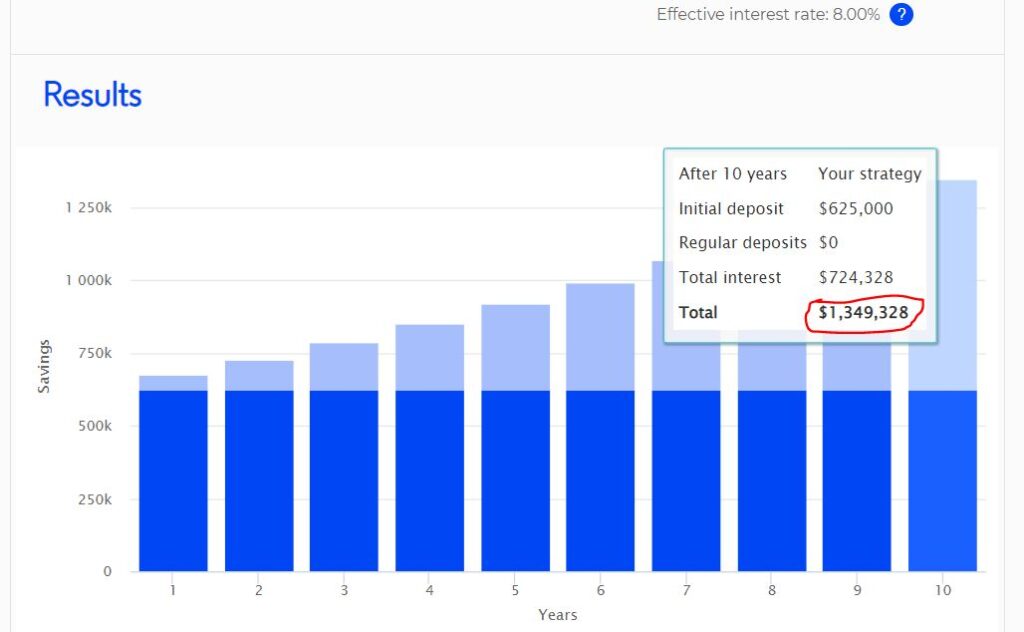

Our FIRE number is $1.25M which will generate $50K per year based on the 4% rule.

Let’s assume that we get to the $1.25M, declare FIRE but decide to both work 1 day a week for 8 hours at $30 an hour.

Would you believe that our combined take-home income would be ~$25K a year? That’s half of what we need to bloody live on!

The portfolio could easily cover the rest and here’s the amazing part. Because we wouldn’t need to be drawing down 4% of the portfolio, it could compound away for longer at the higher amount.

Here’s what half of the portfolio ($625K), if left alone, could potentially grow to given an 8% return after 10 years.

~$1.35M is more than our original FIRE number!

And it’s really important to realise that we only worked one 8 hour day at $30 an hour in this example. You could imagine how dramatic the modelling changes if you worked an extra day or charged a higher hourly rate.

There are two main points here.

- You’re almost certainly going to be earning money post FIRE

- The 4% assume no extra income ever. This is extremely unlikely if you reach FIRE in your 20’s, 30’s, 40’s or even maybe 50’s.

9. Find your ‘enough’

Joseph Heller, an important and funny writer

now dead,

and I were at a party given by a billionaire

on Shelter Island.

I said, “Joe, how does it make you feel

to know that our host only yesterday

may have made more money

than your novel ‘Catch-22’

has earned in its entire history?”

And Joe said, “I’ve got something he can never have.”

And I said, “What on earth could that be, Joe?”

And Joe said, “The knowledge that I’ve got enough.”

— A poem for The New Yorker in May of 2005 by Kurt Vonnegut

I honestly think there’s something in our DNA as humans to always want more.

It has to be some sort of evolutionary trait right.

Imagine two homo sapiens coming across an enormous fruit tree bearing 50 ripe Apples.

The first human decides to only eat enough to be full and then leaves.

The second human gorges themselves and then picks and carries as many as they can hold back to camp with no consideration of others.

Which personality traits do you think has the better chance of surviving and passing on their genes to the next generation? As unfortunate as it is, selfishness is rewarded in the animal kingdom. I know it’s hard to imagine with all our fancy pants technology and civilisation, but we’re not actually that far removed from our prehistoric ancestors and evolution hasn’t yet caught up to deal with the current situation we find ourselves in.

Most of us are hard-wired to always want more.

But you’ll never become FI if your desires and wants continue to increase forever.

Think back to lesson one “The goal is to be happy”.

If you desire something and you don’t have it, this usually results in a feeling of unhappiness. And there are only two ways to fix it.

- You work hard and get what you want.

- You find happiness elsewhere and stop wanting it.

Depending on how exorbitant your wants and desires are, option 1 could mean many decades climbing the corporate ladder working 70+ hours weeks to fund your:

- 3,000sq m Toorak mansion

- 6 beds, 5 bathroom holiday house in Byron Bay

- 5 cars

- 3 jet ski’s

- And so on

Now I don’t want to be judgemental here. If you really want all those things and think the work required is worth it. Sweet. Go for it. Everyone is different.

But if you’re reading this article, odds are that you’re more attracted to the idea of living a simple yet great life that prioritises freedom, autonomy, health, relationships and ultimately happiness.

Figuring out what your ‘enough’ is takes a long time. This is partly because our wants and desires evolve as we get older and our circumstances change.

I for example, never really put too much value in travelling before 2019. I’d been on a few trips here and there and whilst it was good fun, I used to think that international travel was insanely expensive and overrated. Travelling around the world and living in the UK for 2 years completely changed my outlook on a lot of things and broadened my horizons. I now consider travelling to be part of our lifestyle and something we will need to factor into our numbers.

And even though I think a little bit of lifestyle inflation is perfectly normal and healthy, you’ll never have peace of mind until you discover your ‘enough’.

If you don’t figure it out, you’ll always be wanting more.

10. We’re all dealt a different hand in the game of life

There’s a quote that I can’t seem to find that loosely goes like this.

A CEO was perfectly happy with their $1M bonus until they found out a competitor CEO received $100 more

Comparisons. We’re all guilty of making them.

And the messed up part is sometimes we were happy until we see what someone else has.

It happens all the time and is part of the reason I’ve disconnected all of my social media accounts.

Practising the art of gratitude can be really helpful to remind yourself of all the great things in your life. But we’re humans and I’ve fallen victim to unrealistic comparisons a bunch of times. It’s perfectly natural to stumble across someone who you may have gone to school with and be jealous of the life they’re living now.

What I’ve come to realise after hearing from literally thousands of Aussies on their way to FI is that there can be a gigantic gap between peers within the same cohort. I’m talking about the advantages and disadvantages between two people who on surface value seem to be pretty equal.

There’s a great book called Outliers by Malcolm Gladwell that explains just how incredible one little advantage early on in someone’s life can completely change their trajectory.

Did you know that 40% of the best hockey players in Canada are born between January and March?

This is no coincidence. It turns out that in minor league hockey, children are grouped by birth year and players born in January are, on average, bigger and taller than December-born players.

This seemingly unimportant attribute gives players born in the first months of the year a head start that turns into a lifelong advantage.

That one little leg up can have the following flow-on effects:

- They are bigger and stronger than their peers which makes hockey easy for them

- They are noticed by coaches and identified as a good player. Extra coaching or special treatment may be given

- They will most likely be chosen to represent their squad team which means more playing time against a higher level of competition and access to better coaching

- They continue to get extra playing time against elite competition with the best coaches in the country year after year

These sorts of advantages happen all the time and compound throughout one’s life.

The same is equally true for disadvantages.

But it’s really hard to know what cards a person has been dealt even if you know them quite well. And it’s almost impossible when reading a stranger’s blog or listening to a guest on a podcast.

The goal of FI is a mastery of money that’s a personal journey.

A little bit of healthy competition can be good but never feel inadequate when you come across someone similar who seems to have it all figured out. They may have been dealt two aces.

The reverse is also true.

We have no idea what has happened in someone’s life that has influenced the position they’re in now.

In summary, compete against the person in the mirror.

Wake up each day trying to be a better version of yourself.

Because…

“Comparison Is the Thief of Joy”

— Theodore Roosevelt

That’s a wrap! 10 the biggest lessons I’ve learned over the past 10 years pursuing FI!

I’d love to know what was your favourite lessons in the comment section below 🙂

As always,

Spark that 🔥

by Aussie Firebug | Jan 7, 2022 | Net Worth

I publish these net worth updates to keep us accountable, have others critique our strategy and show that reaching financial independence in Australia is very doable without winning the lotto, having a high paying job or inheriting a wad of cash. The formula to be able to retire early is simple, the hard part is being consistent and sticking to a plan for many years. The table at the bottom details our entire journey from being $36K in debt all the way until we reach 🔥

And that’s a wrap for 2021!

It’s wild to think that we are already in 2022, just like that meme, I feel like I am still processing 2020 🤯

December was here and gone in a minute for the Firebug household. So many Christmas breakups, family gatherings on both sides, friends coming back to town for the festive season, birthdays, NYE events and so on.

We hosted the annual Christmas day breakfast at our new home this year too. I recently bought a new barbie (I’m obsessed) and really wanted to put it to work.

This is living 🙌😍

I basically have started to barbeque just about everything now. And when the weather is good, it’s damn hard not to crack open a beer. I’m usually pretty strict with alcohol on work nights but I don’t know what it is about barbequing that makes me break the rules. I might have to start buying some non-alcoholic beers to lessen the effect 😅

Mrs FB had a hectic finish for the school year (as is always the case), but is super pumped about dropping down to 4 days a week starting next year 🎉🥳.

2021 was such a whirlwind of a year and I’m stoked that we managed to tick off all the major items we had on our list like buying a house and tying the knot.

Thanks a lot to everyone who reads the blog/listens to the podcast. I’ve got some great ideas for AFB and the Aussie FIRE community in 2022 that I can’t wait to share with you all 👊

Net Worth Update

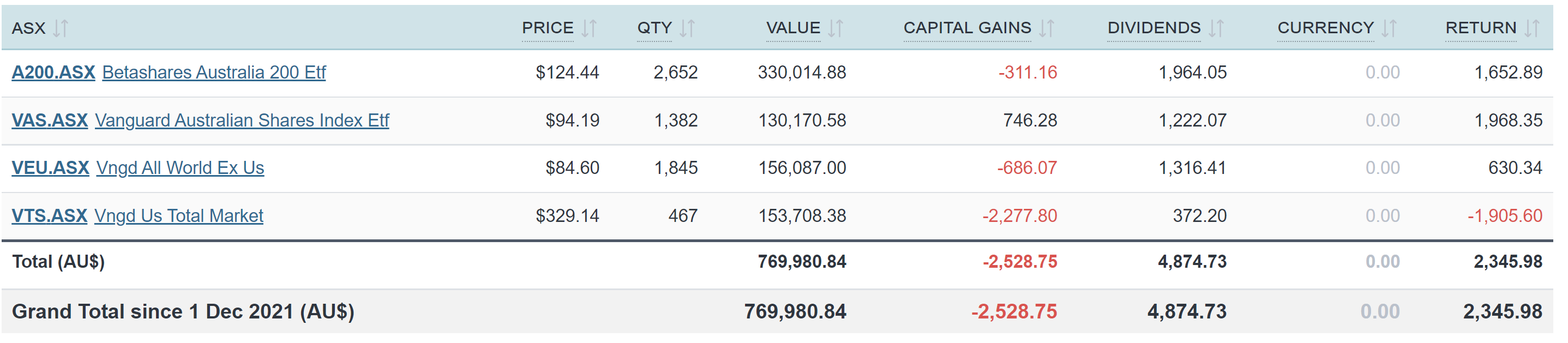

So we lumped summed ~$210K into the markets in late December/early January. This was surprisingly difficult for us to actually pull the trigger.

The general consensus in the FIRE community is to not get caught up in timing the market. This is easier said than done.

I’m human just like the rest of you and I also read a fair bit of finance mumbo jumbo content too. It’s fun to read opinion pieces and I’ll watch the occasional YouTube video of some doom and gloomer who has put together a pretty slick video with nice editing on why the next recession is about to drop.

The hardest part mentally was the markets being at an all-time high (or close to it). No matter how much I read that it doesn’t matter if you’re in it for the long term, it’s still bloody difficult not to wait for a dip.

So I waited right until the end of December before we invested our lump sum. And right on cue, the markets had a slight tumble afterwards 🙃🔫.

We would have been so much better off if I had just invested that money straight away but such is life. And the downturn right after we invested $210K is a major reason the net worth only grew by $2K in December. The other reason was a pretty expensive month.

The FIRE portfolio actually went down slightly in December due to the market dip after our big investment. December was really expensive for us too with Christmas/holidays.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

Shares

The above graph is created by Sharesight

We’re all in baby!

$769K all in shares which blows my mind!

Man… it wasn’t too long ago that I was in my mid 20’s and reading US FIRE blogs on a daily, dreaming about reaching financial independence someday in the future. I can’t remember whose blog I was reading but they had just hit $700K in shares and I remember being awestruck by the figure.

It just seemed like so much god damn money to have invested. I thought it was going to take me forever to get anywhere near that amount.

So to see $769K on the screen is a bit surreal to be honest.

But on the flip side, finally investing all that money felt like a weight off our shoulders. It’s in the market now so whatever happens, happens. If there’s a huge recession in 2022… well… that would suck but we’ve just accepted that and it’s back to business DCA’ing each month which is so much easier to do.

We made three huge (for us) purchases in December/early January.

- $53K into VTS

- $62K into VEU

- $95K into A200

This brings the portfolio into the following splits

60% Aussie 40% International

and

43% Betashares 57% Vanguard

Some of you hawkeye readers may have noticed that this is slightly different to our latest strategy explained article (2.5). I’m actually going to write another updated strategy explained article because our investing strategy is very fluid and changes based on our current circumstances and priorities.

There are no major reasons why we went with the splits above, it’s just what we feel comfortable with atm. We also like to spread the management risk around by having a decent chunk of our portfolio in Betashares and not just Vanguard. It also helps that A200 is cheaper than VAS atm too.

Looking forward to hitting the $800K mark in the not so distant future 😁

Networth